Today, I will share my step-by-step method to answer how much house can I afford. This is part 2 of the FatFire House series. Read part 1 here.

Whether you’re a renter today, a homeowner, or a retiree, this guide will help you decide whether to move or stay.

We’ll first understand the myths and lies, then learn how to use your net worth goal to calculate how much house can I afford.

Let’s get started.

The Myth of Home Ownership

Buying a house is a big decision, financially, emotionally, and socially.

Financially, a house is the most expensive thing you’ll ever buy. It’s so costly people take 30 years to pay it off.

Emotionally, buying a house is a significant milestone and a source of pride. You are growing older, building a family, and settling down.

And socially, buying a house is an ego-driven status game. You might feel pressured to buy a home as large as your siblings, coworkers, or friends. Perhaps a place that symbolizes your success?

I recognize it’s not easy to decide how much house can I afford. The answer is financially involved and emotionally and socially sensitive.

We’ll break it down, one by one. Let’s start with the financials.

The Financial Scam to Own a Home

The housing industry is a trillion-dollar industry.

It’s an industry made up of banks lending consumers mortgages and real estate developers selling houses you cannot afford.

Here’s an example of lies they tell:

This real estate agent shares the benefits of buying a house on Instagram. I have debunked these claims in part 1 here.

This person probably doesn’t even understand economics, but she’s saying these things because she makes 6% of every house sold. So of course she wants to you to think you can afford a big, expensive house.

Don’t fall for these lies.

Home Ownership and Consumer Debt

Just do a quick search on Google or Instagram and you will be inundated with all kinds of peer and social pressure to buy a house.

It is exhausting… but it is working.

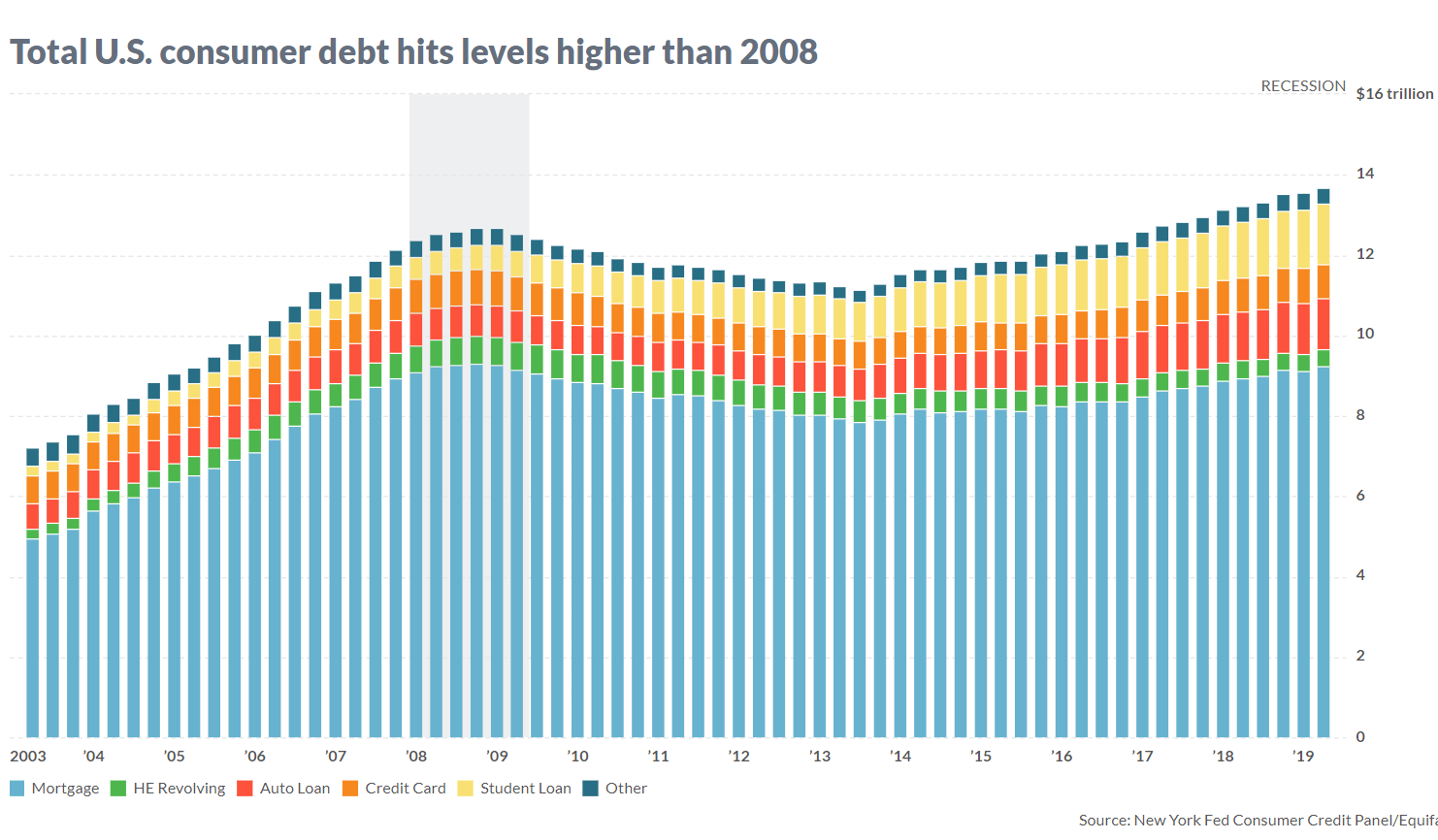

Today, Americans are ten trillion dollars in debt from home mortgages.

This graph shows mortgages are by far the majority of Americans’ household debt.

Americans buy expensive homes because industries of companies make money from your spending.

A Rented Home is a Real Home

Renters are not temporary residents of a community; they are residents and community members whose homes should be just as special.

We have to change the perception that a rented home is not a real home.

With the right landlord and the right rental, you can create everything you want for a home without paying the prohibitive price tag.

It takes a mental shift more than a financial change here.

Just like how couples think they can’t be happy without a diamond ring or a huge wedding, the real estate industry brainwashed us to believe great memories only happen in large houses.

We forget what children all know: happiness is not about where you live or what you have but who you’re with and how you make it.

You’re not going to be any happier than you are right now right here.

If you rent, make your apartment as unique as a place as if you own it. Make it homey, decorate it carefully, and make it the home you deserve.

Seek Wealth, Not Money or Status

I am a fan of Naval. He is a tech entrepreneur, and he advises people to seek wealth, not money or status.

Buying a big house is the ultimate status-seeking act.

Wealth is an asset that keeps growing while you sleep.

Wealth is owning a company, either directly or indirectly via stocks, that works hard without you working hard.

A house can also be a form of wealth if you can rent it out, but you’ll probably get more returns putting your money elsewhere like stocks.

House, above the necessary comfort level, is just a status game.

Real Estate is a Status Game

Architectural Digest and Celebrity House Tours are all status games.

Don’t play the status game.

Status games never make you happy, fulfilled, or better.

How do you know if you’re already playing the house-buying status game?

Ask yourself, are you buying a house because:

- Everybody else is buying a house?

- Living in a beautiful house makes you happier?

- You’re at the age where you “should” buy a house?

- Do you want to “invest” in a house?

If you answered yes to any of the above, then you’re playing the status game.

Because:

- Copying others rarely make you happy

- A pretty house isn’t going to make you happy

- It’s a marketing scam that you should ever buy

- Real estate is not a good investment.

Don’t seek the status game.

Only buy a house that you can afford and need.

Home Ownership and the American Dream

George W. Bush once said, “Right here in America, if you own your own home, you realize the American dream.”

Connecting the American dream to homeownership is the most brilliant marketing strategy.

And it is also a myth.

The U.S. is built on materialism: what we buy is who we are: houses, diamond rings, cigarettes, guns, teslas, the list is endless.

The mortgage industry said, “the American dream means homeownership,” even if it means you borrow money for the next 30 years to make banks rich.

So let’s be clear: the American Dream is not homeownership.

The American Dream is living a fulfilling life: and you cannot buy your way into a fulfilled life.

Prettier Homes, Happier Life?

For whatever reason, people think those who live in beautiful homes are happier people.

After all, what would these people fight about if they are living in luxury?

It turns out that many wealthy people living in fancy houses are depressed, miserable, and drowning in debt just as much as the next person.

A fulfilled person is a person free to do whatever they want with their time.

And wealth gives you the freedom to do whatever you want.

So a prettier home doesn’t give you a happier life. It’s not wealth.

Seek wealth. Not a prettier home.

Real Estate Addiction

Social media makes many people depressed because they can’t fathom why everyone’s life is more fabulous, happier than theirs.

The latest addiction is real estate addiction.

People continuously look at magnificently staged real estate listings on Zillow, imagining how much happier they’d be if they just lived in these immaculate houses.

It is making them sadder and jealous. It’s not reality, but the internet makes people want to buy a house they can’t afford just to play the status game.

Obsessively browsing real estate listings, believing that’s happiness is no different from looking on Instagram, thinking everybody is happy.

A home is what you make of it. You can make a cheap rental more special than a multi-million dollar mansion.

Oh, and kill that Zillow or Redfin app on your phone, now. It is addictive like sugar, cigarettes and Facebook!

Home Ownership and Economic Mobility

Consider this: high achievers mostly leave their hometowns and move around often.

People who build up skills to make money and achieve financial independence tend to rent.

In this sense, buying a house may lock you down unnecessarily early, not giving you the flexibility to make more money.

So ask yourself, “will buying a house limit my options?”

Where Can You Afford to Live

But if you decide you want to buy a house, the second step is to choose where to live.

I recommend you don’t buy a house unless you plan to live in the same place for the next ten years.

That’s right; you need to live in a house for over a decade for the money to be worth it.

Living in a house for only a few years means you’ll be dumping a lot of money toward interests and nothing toward paying down your principal.

The real estate agent fees to inspect and close are also expensive. If you pay all that money only to live in a house for five years, then you might as well rent.

Minimize Commute

We choose to minimize our commute time to under 30 minutes from work because time is the most precious thing.

When our commute time went down to zero during the pandemic, I realize I should never have to commute ever again.

With a 30-minute commute each way, I am already wasting weeks of our life every year just going from home to work.

I’d much rather save that time and spend it doing things I love.

So before you buy a house, consider the commute.

Houses and School Zones

One of the most important things that people often overlook is the school zone.

And if you plan on having children in the next ten years, this is still relevant for you.

Ask yourself, “are we sending our children to a public school or private school?”

If you’re sending your children to a public school, you have to make sure the house you buy is in the right school zone.

Excellent public school districts in the United States have costly houses.

Or, consider buying a house in a very cheap neighborhood with a bad school and send your kids to a magnet school or private school.

I live in an area where the top public school zoned houses cost at least a million, most likely two million dollars.

I did some quick math and realized it’s cheaper to send our kids to private schools.

Diverse Neighborhoods

You’d also want to consider the diversity of where you live.

This isn’t just relevant for people of color; this is relevant for everyone, especially white people.

It’s everyone’s responsibility to branch out and make friends with those who are different from us: politically, racially, economically, physical, and mental capability wise, and sexual orientation.

And you’ll only be able to do that if you live closer to a large city. So this is definitely my opinion talking here.

This can be hard because most of the affluent neighborhoods in America with great schools are exceedingly white.

We use https://polarislist.com to find excellently ranked, diverse schools, with diversity indicated by a high percentage of students receiving free and reduced school lunches.

The Best and Most Diverse High Schools in America

Here is a list from Polaris of the most diverse AND academically rigorous schools in the United States:

| # | High School (Diverse) | Location |

|---|---|---|

| 1. | STUYVESANT HIGH SCHOOL | NEW YORK, NY |

| 2 | BOSTON LATIN SCHOOL | BOSTON, MA |

| 3 | BRONX HIGH SCHOOL OF SCIENCE | BRONX, NY |

| 4 | CAMBRIDGE RINDGE AND LATIN | CAMBRIDGE, MA |

| 5 | MONTGOMERY BLAIR HIGH SCHOOL | SILVER SPRING, MD |

| 6 | BROOKLYN TECHNICAL HIGH SCHOOL | BROOKLYN, NY |

| 6 | RICHARD MONTGOMERY HIGH SCHOOL | ROCKVILLE, MD |

| 8 | TROY HIGH SCHOOL | FULLERTON, CA |

| 9 | JOHN P. STEVENS HIGH SCHOOL | EDISON, NJ |

| 10 | ARCADIA HIGH SCHOOL | ARCADIA, CA |

| 10 | INTERLAKE SENIOR HIGH SCHOOL | BELLEVUE, WA |

| 10 | NEWTON NORTH HIGH SCHOOL | NEWTONVILLE, MA |

| 13 | HURON HIGH SCHOOL | ANN ARBOR, MI |

| 14 | CYPRESS BAY HIGH SCHOOL | WESTON, FL |

| 15 | FIORELLO H LAGUARDIA HIGH SCHOOL | NEW YORK, NY |

| 15 | SUNCOAST COMMUNITY HIGH SCHOOL | RIVIERA BEACH, FL |

| 17 | UNIVERSITY HIGH SCHOOL | IRVINE, CA |

| 17 | WHITNEY M. YOUNG MAGNET HIGH SCHOOL | CHICAGO, IL |

| 19 | MENLO-ATHERTON HIGH SCHOOL | ATHERTON, CA |

| 20 | EASTSIDE HIGH SCHOOL | GAINESVILLE, FL |

| 20 | NORTH HOLLYWOOD SENIOR HIGH SCHOOL | NORTH HOLLYWOOD, CA |

| 20 | WALTER PAYTON COLLEGE PREPARATORY HIGH SCHOOL | CHICAGO, IL |

These high schools come from across the country, but tend to be near metropolitan areas in costal states.

The good news is that many of these schools are exam schools so it doesn’t matter where you live. The bad news: your kid has to get into them.

- New York City (4 of the top 20)

- Massachusetts (Greater Boston) (3 of the top 20)

- California (Great LA and SF Bay) (5 of the top 20)

- Maryland (Greater DC) (2 of the top 20)

- Washington (near Microsoft HQ)

- Michigan (near University of Michigan)

- Florida (Greater Miami) (3 of the top 20)

- Illinois (Greater Chicago) (2 of the top 20)

- New Jersey (NY Suburb)

The southern states have elite schools too but they tend to be more homogenous and less diverse.

Housing Affordability Based on Net Worth

Once you’ve decided “I want a house”, let’s discuss “how much house can I afford”.

Consider these two questions I get all the time:

- I make $45,000 a year. How much house can I afford?

- I make $70,000 a year. How much house can I afford?

Legal advice says you should not spend more than 28% of your monthly gross income on a mortgage. Or that your total housing cost should not exceed 36%.

Other traditional advice says you shouldn’t buy a house that is more than 2.5 times your annual salary.

These are all good advice, and you should follow them. But a salary-based rule of thumb is not enough for financially independent people.

Instead, you should look at your net worth goal and buy a house that is less than 17% of your net worth goal.

Why? Because having a high income is not necessarily going to make you wealthy.

Income means nothing if you can’t save it, invest it and turn it into wealth (or net worth).

The only measure of wealth is net worth.

Net Worth and Housing Affordability

Use net worth to estimate how much house can I afford.

Net worth is the ultimate signal of how wealthy you are. The wealthier you are, the more expensive a house you can afford.

If you are close to retirement or on the path to financial independence, you probably already have a net worth goal in mind.

This goal probably took into account your salary and other things, such as your savings rate and investment growth rate.

Many fatfire families have a net worth goal of $4 million, which means they can afford a house that is $680,000, or 17% of the $4 million net worth.

If your financial independence number is $1 million, then you can afford a house that is $170,000, or 17 percent of 1 million.

Live and Buy Like the Top 1%

Why 17%, you might ask?

Wealthy people have a primary residence that is only a small share of their total net worth.

The table below shows the average net worth percentile of a family and the percentage of net worth from primary residence.

The 99th percentile is the people in the top 1%. The 50% percentile are people in the middle. The 25% percentile are the people who are in the bottom half of the net worth spectrum.

| Net Worth Percentile | Primary Resident as % of Net Worth |

|---|---|

| 10th percentile | Cannot afford a house |

| 20th percentile | Cannot afford a house |

| 30th percentile | 97% |

| 40th percentile | 93% |

| 50th percentile | 78% |

| 60th percentile | 66% |

| 70th percentile | 54% |

| 80th percentile | 36% |

| 90th percentile | 18% |

| 99th percentile | 7% |

The chart above shows the 99th percentile (the top 1%) has 7 percent of net worth in the primary residence.

For the top 1% with $20M, they can own a $1.4M house.

The 90th percentile (or the top 10%) has 18% of their net worth in their primary residence.

Everyone should aim to become the top 10%.

And this means you have to live like the 90th percentile people.

And therefore, never spend more than 17% of your net worth goal in a house.

Most People Overspend on Houses

These days, it is almost universally better to rent than to buy in nearly all major cities in the United States.

The situation might be different if you live in rural areas or the suburbs.

Americans with a median net worth, or 50th percentile, have 78% of their net worth in their primary residence!

This is why most Americans can never retire. The majority of their net worth is tied to their primary residence, not to investments!

Below is a chart that translates your net worth goal into how much house can I afford:

| Target Net Worth | House Cost (17% of Net Worth) |

|---|---|

| $250,000 | $42,500 |

| $500,000 | $85,000 |

| $750,000 | $127,500 |

| $1,000,000 | $170,000 |

| $1,500,000 | $255,000 |

| $2,000,000 | $340,000 |

| $2,500,000 | $425,000 |

| $3,000,000 | $510,000 |

| $7,000,000 | $1,190,000 |

| $11,000,000 | $1,870,000 |

So if you wonder what salary you need to afford a $700K house, you are thinking about it in the wrong way.

Instead, know that you need to plan to reach $4 million in net worth if you want to afford a $700K house.

To reach $4 million in net worth, you need not only a good salary but an even better investment strategy that is balanced and focused on the long term.

If you don’t know your net worth goal or don’t plan to achieve it, you are not ready to buy a house.

You Qualify for Too Much Mortgage

Chances are, if you ask the bank how much mortgage you are qualified for, they are going to give you the wrong number: most of the time, too high, but sometimes too low.

Banks use your salary to determine your mortgage qualification. So how much mortgage you can qualify for is only dependent on your paycheck, not wealth.

The housing industry wants you to overspend on the house as long as you can keep paying them money!

They will reject people who obviously will default but accept your application as long as they think you won’t default on their loans.

But they don’t care if you are putting too much money toward the house.

So don’t fall for the trap.

Stick to make sure your net worth is less than 17% of your net worth goal.

25% Down Payment and 1-Year Contingency

Also, make sure you have enough cash to pay for a 25% down payment.

Many people only put 10% down. I think that’s too low.

You are going to pay too much interest.

Even if a bank qualifies you for a 10% down, don’t take it.

Next, you should have cash on hand to pay for one whole year’s mortgage plus other costs of living expenses.

This way, even if you stop having any income for a year, you will still pay the mortgage and not have the banks seize your house.

Pay Off Credit Card Loans First

You should not buy a house if you have credit card debt.

End of story.

Pay off your credit card debt as soon as possible before you invest or do anything else, including buying a home.

It is okay to buy a house with student loans, but you should be realistic and make sure these loans, when added together, are manageable to pay off.

How Much House Can I Afford: Summary

The housing industry is lucrative.

It puts out marketing scams pinning us to play the status game of “who has the bigger house” against each other.

And just like how Instagram photos are fake, those beautifully staged home tours, and Zillow photos are also manufactured.

A vast, pretty house will never make you happy.

You’d be surprised how a decent apartment can be such a pleasure to live in if you just put in a more effort to decorate and make it your home.

And if you want to buy – make sure you find a place that minimizes your commute and takes into account your education plans for your children.

Always aim to buy a house that is less than 17% of your net worth goal.

This way, you can live like the top 10% and put the majority of your net worth in stocks to grow toward fatFIRE.

What’s Next?

Read Part 1 of the Fatfire Housing series: Stocks vs Real Estate: Never Buy a House as Investment

No longer buying a big house? Check out what I do with 10% of my net worth: What are the Best Stocks to Invest Long Term?

Stop browsing Zillow and learn to live a better life in my ultimate guide on How to Be Healthy and Live Forever