This is the first of a two-part guide to tell you everything you need to know about the 401K contribution and 401K scams.

In this guide, I’ll cover what is a 401K plan, 401K contribution limits, IRA vs 401K, and exactly why you should max out your 401K contribution.

In the next guide, I’ll cover why there are also many 401K scams you need to avoid.

What is a 401K Plan? How Does it Work?

A 401K plan is a financial investment plan your employer set up. It is the most important part of your FIRE journey.

Both you and your employer contribute money to this plan for you to use during retirement.

The 401K plan is wildly popular and heavily adopted. Just check out these numbers below according to the Bureau of Labor Statistics:

- 70% of company workers have access to retirement benefits

- 55% of company workers participate in retirement benefits

- 79% of company workers who have access to them participate in them

How much can you contribute to 401K?

How much can I put in my 401K, you might ask?

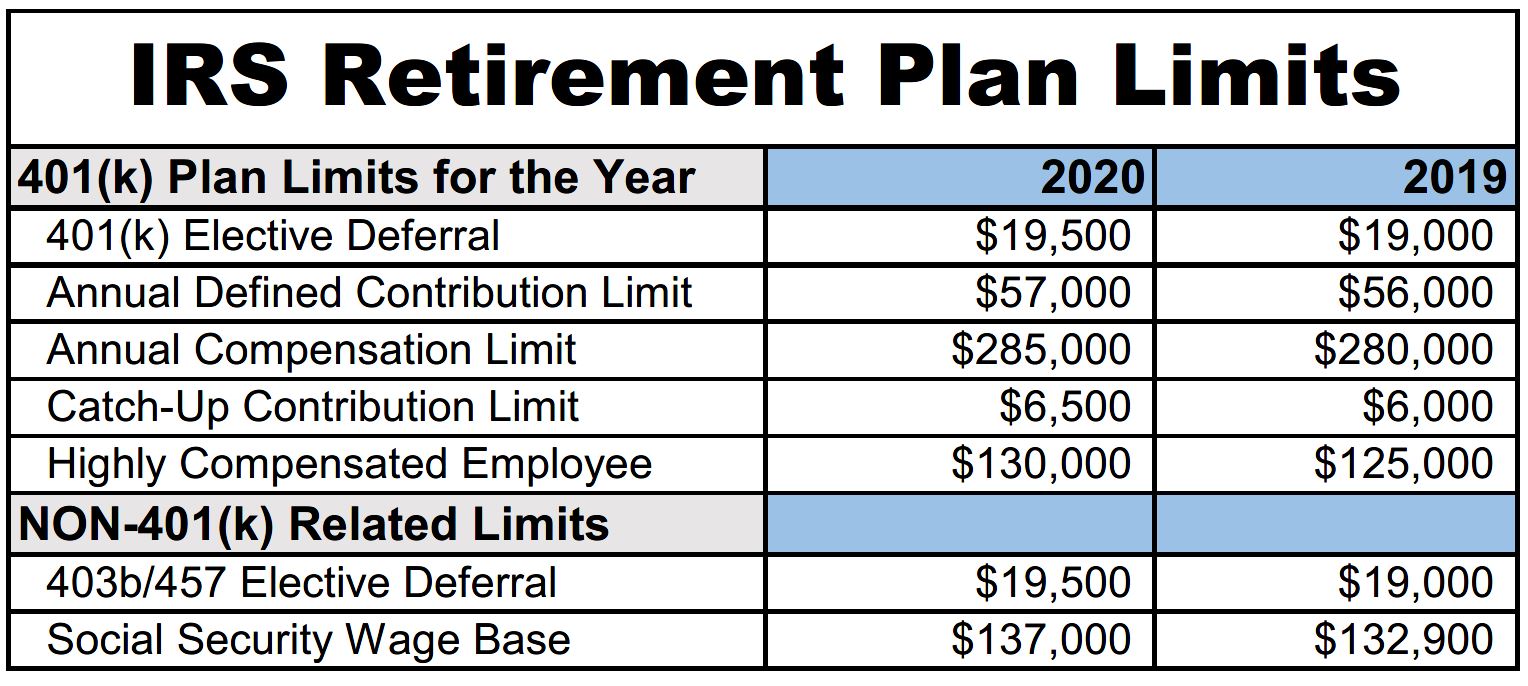

The IRS regulates the 401K, and according to IRS rules, the max 401K contribution for 2020 is $19,500.

The 401K contribution limits have been steadily increasing. The 401K contribution limit in 2018 was $1850, in 2019 it was $19,000, and in 2020 it climbed again to $19,500.

$19,500 is not only the 401K max, it’s also the max for other retirement plans such as the 403(b), most 457 plans, and the federal government’s Thrifty Savings Plan.

When Can You Withdraw From 401K?

The IRS regulates 401K withdrawal rules that decide when can you withdraw from your 401K plan.

In general, the IRS wants your 401K money to be off-limits until you retire.

So they want to come up with a rule that delays your 401K withdrawal until after you retire.

The current 401K withdrawal rule states you can withdraw from your 401K when you turn 59 and ½ years old.

What happens if you withdraw your 401K before you turn 59 and ½ years old? Then you will get an early withdrawal that equals 10% of your withdrawal amount. So don’t do it!

401K minimum distribution (When must you withdraw?)

The IRS also wants to make sure you withdraw your money before you die.

So it also has a required minimum 401K rule.

The 401K RMD rule states that you have to start withdrawing when you turn 72.

Furthermore, the 401K RMD stimulates that you have to withdraw at least your RMD number, a number that is calculated by dividing your account balance over a life expectancy factor.

For example, if you have an account balance of $600,000 and you are turning 72 this year, then the 401K RMD rule says you must withdraw at least $22,641 from your 401K this year (600000/26.5=22,641).

The 401K RMD penalty can be severe, sometimes equaling 50% of your required minimum distribution amount.

So make sure you get your money out when you are old enough. Fidelity has a super useful RMD calculator and table, click here to. check it out.

401K contribution limits with employer match

The best part of a 401K is that employer match.

Your employer is required by the IRS to have some kind of employer match.

It’s also important to know that your employer match does not count toward your individual 401K contribution limit (the $19,500 in 2020)

Between your 401K contribution max and employer match, your combined maximum contribution to your 401K is $57,000.

Yes, this means an employer can contribute $37,500 to your 401K, but very few would give you anywhere near the employer match max.

Consider yourself lucky if your employer matches 3% of your salary.

An employer match of 3% of your salary means the employer will match what you put into your 401K, dollar-for-dollar, up to an amount that equals 3% of your salary.

So if you make $60,000 a year, and you put at least $1,800 into your 401K, your employer will also contribute $1,800 to your 401K.

But if you put less than $1,800, your employer will match you up your 401K contribution and no more than that.

And if you put in more than $1,800, your employer will still contribute only $1,800.

How much should I contribute to 401K?

Ever wonder how much should I contribute to my 401K? To answer this question, let’s look at what benefits 401K provides us.

First, imagine you don’t have a 401K.

Imagine you’re investing your money from a savings account into a mutual fund. In this case, your invested money will be taxed in three ways:

- Assuming your savings money came from your paycheck, you have already paid income tax on it. Your income tax could be as high as 37% per year.

- If your mutual fund has sold and bought stocks (most likely it will) this year then you may have realized capital gains and thus must pay capital gains tax.

- If your mutual fund has dividend stocks then you will have to pay dividend taxes every year on the dividends received.

This can all add up to be a lot of money being paid to taxes.

And that’s where the 401K comes in.

When you invest your money via a 401K plan, you defer paying all three of the taxes above until withdrawal.

The money you save on taxes leaves you with more money to invest and over time, the cumulative savings can be a huge difference in your net worth.

Because of these incredible tax savings, the answer to the question “how much should I contribute to my 401K’ is always to contribute to the 401K max.

To be clear, your 401K contribution will still count as part of your gross income. So you still have to pay Medicare, FICA, Unemployment and Social Security taxes on your 401K money.

But you don’t have to pay federal income on your 401K contributions until withdrawal.

401K Tax Deduction

The 401K not only defers income tax, it also delays dividends and capital gains tax until the money is withdrawn.

Dividends taxes are the same as income taxes and can be as high as 37%. If you don’t have to pay dividends taxes every year, you can reinvest more of your dividends back into your investment, and over time, it’ll make a huge difference in your growth.

Capital gains taxes are either short-term (if sold within 1 year) or long-term. Short-term capital gains taxes are also the same as income taxes.

Long-term capital gains taxes are either 0%, 15%, or 20% depending on your income.

You might also get taxed an additional 3.8% for having an income of $200,000 or above.

So even long-term capital gains taxes can be high (23.8% for high incomes).

The savings from all taxes, both the income tax and recurring dividend and capital gains taxes are why the 401K plan is so attractive and necessary to your financial freedom.

How Much Should I Have in My 401K?

What is the average 401K contribution in the U.S.?

Given the incredible tax savings from the 401K plan, Americans are not contributing nearly as much as they should.

On average,

- Baby boomers contribute < 12% of their gross income into a 401K plan.

- Generation X contributes just below 10% to their 401K.

- Millennials, hit hard by the 2008 recession, contribute less than 8% to their 401K.

Only 41% of households have a 401K in the United States. The average 401K balance of the retired is under $200,000, while those in their 30s have less than $50,000 in 401K.

These are bad numbers:

And that’s why older Americans are increasingly filing for bankruptcy because they can’t afford out-of-pocket Medicare bills.

Also why Younger Americans are still living with their parents into their 30s and very few are buying homes.

Is our 401K contribution enough for retirement?

A 2018 report from the Stanford Center on Longevity says that if you want to retire at all, you should invest at least 10% to 17% of your income.

Anything below 10%-17% of 401K contribution means you won’t be able to survive through retirement.

And if you want to FIRE or fatFIRE, I recommend you contribute more.

Specifically, I recommend that ambitious people always contribute at least 50% of your income into savings across 401K, IRA, and any other investment accounts you have.

In our household, we contribute nearly 70% of total gross income to savings.

How do we do this?

- We rent even though we can afford a million-dollar home. This saves a lot of money on home maintenance, real estate taxes, and mortgage.

- We drive a Honda with 200,000 miles on it even though we could afford a Tesla.

- Our only luxury spending is on fine dining.

- We don’t have a maid or nanny. (Although this might need to change soon…)

I argue in this post that women and people of color have it worse and rather than waiting for society to upgrade, I advocate that we advocate ourselves along with anyone else who is ambitious and determined.

So whether you are rolling in the dough or struggling from paycheck to paycheck, you can always spend less and save more.

So challenge yourself today by making a budget or opening a Personal Capital account.

No matter your circumstance, you can build a pro wealth mindset and invest through the highs and thrive through the lows.

And always max out your 401K. Maxing out 401K every year since your 20s might just take you to FIRE before you know it.

How Long Will My 401K Last?

Wondering how long will your 401K last you through retirement? Use the 4% rule.

The 4% rule states that you should not spend more than 4% of your money every year.

So if you have $500,000 in retirement this year, the 4% rule suggests that you only take out $20,000 that year.

As long as your spending does not exceed the 4% rule, your 401K will last you a long time.

However, there are two things to watch out:

- The 4% rule does not take into account taxes. So if you can only take out $20,000, remember that you might have to pay taxes on that money and will end up with less than $20,000 to spend.

- The 4% rule was created during a time when the stock market was roaring. For most conservative investors, they actually assume a 3% or even 2.5% rule.

As you can see, even if you have a million dollars in the bank, you only can withdraw $40,000 per year in order to make sure you don’t outlast your 401K and go bankrupt.

And if you want to calculate future incomes beyond the first year, be sure to take into account inflation.

And this is why you should max out your 401K every year for as long as possible.

How much should I have in my 401K?

Let’s calculate how much you need to have in your 401K by using an example.

- First, determine your monthly expenses during retirement. Make sure this number is generous and includes any one-time fees, out-of-pocket emergencies, and vacations.

Let’s say that you think you need $5,000 a month.

- Now, subtract what you think you’ll get in social security benefits.

Let’s assume you’ll get $1,500 in monthly social security

$5000-$1,500 = $3,500, money to make up from your retirement.

- Now let’s annualize this number, and include taxes. Assume your tax rate will be 15% – higher than paying no taxes, but less than the highest tax brackets.

(3500/(1-0.15)*12 = $49,412.

You’ll need to take out $49,412 from your retirement account every year in order to pay for taxes and still have $5,000 left to spend after subtracting social security.

- Determine much should you should have in your 401K using the 4% rule.

49412/0.04 = $1,235,294.

You’ll need a bit over a million dollars in our retirement account to fund a retirement life of $5,000 a month with $1,500 from social security.

If you think the amount you need is higher than you think, you are not alone. It takes a lot of wealth to fund a retirement well into your old age.

And that is why people should always max out your 401K and IRA whenever you can.

Best Investment Fund for 401K Contribution

It’s not enough to max out your 401K, you have to invest it in the right fund.

I prefer to max out 401K with index funds from Vanguard – here’s a list of my favorites.

And my #1 go-to mutual fund for 401K, the one where I max out my parent’s 401K money into, is the Vanguard Wellington Fund.

It is a perfect 401K fund for those who are close to retirement and want a balanced portfolio that minimizes risks while maximizing growth.

The Wellington Fund is also perfect for your 401K because it’s actually a bad fund to buy outside of your 401K.

And this has to do with Wellington’s 25% turnover ratio.

A turnover ratio is the percentage of a fund’s holdings that changed over the past year.

The higher the turnover ratio, the more likely you’ll pay capital gains taxes.

This is not a problem when you are invested in a 401K where you delay capital gains taxes until later. But it becomes a problem when you try to buy it outside of a retirement fund.

In fact, Vanguard Wellington is currently only available via a retirement fund like the 401K and closed to personal investors using non-retirement money!

So consider max out your 401K with this 100-year old fund you can’t find anywhere else.

401K vs IRA Contribution

What’s the difference between 401K and an IRA? Is the 401K an IRA?

And should I invest in both? Find out below.

Like 401K, IRA (Individual Retirement Account) is another tax-deferred investment plan.

Americans have roughly the same amount invested in their IRA as they do in their 401K today.

But there are three key differences between 401K and IRA.

1. 401K is Company Sponsored

IRA is not company sponsored. So there is no employer match for an IRA.

The only exception is if you have a SIMPLE IRA or SEP IRA.

A SIMPLE IRA is a 401K plan for small businesses that cannot afford to have a 401K plan due to its heavy rules, regulations, and fees.

The SIMPLE IRA is by far the most common 401K plan for small businesses.

Note: there is also a SIMPLE 401K plan but this is less common.

If you own a business, should you get a SIMPLE IRA vs 401K? I would recommend a SIMPLE IRA.

The SIMPLE RA is much easier to set up and cheaper to maintain. Plus, as we’ll learn later, the IRA has will allow your employees to select any mutual funds rather than a limited list.

2. 401K Contribution Has a Higher Cap Than IRA

The contribution cap for the 401K is $19,500 in 2020.

For IRAs, the contribution limit in 2020 is $6,000 for everyone and $7,000 for older works over 50.

3. IRA Has More Investment Choices than the 401K

The last difference is crucial and favors the IRA more than the 401K.

An IRA has (way) more choices in terms of which investments you can buy.

For example, you can open an IRA account in Vanguard and access thousands of low-fee index funds.

But when you open a 401K with a company, you can only access a few dozen investments, most of them not index funds and have high fees.

This is a major flaw of the 401K plan, and we’ll go into details shortly about how you can avoid getting scammed by high fees and bad funds.

But for now, the takeaway here is that you should max out your IRA even if you max out your 401K.

Roth vs Traditional

The traditional 401K is by far the most common retirement plan.

But since 2006, there is a Roth 401K plan that some companies also offer to their employees.

In the IRA world, you can also buy a traditional IRA or a Roth IRA.

Caveat: when people say 401K or IRA, they default to mean “traditional”. But in reality, 401K can be either traditional or Roth, and IRA can also be traditional or Roth.

Below, let’s talk about the two options: Traditional vs. Roth.

Traditional IRA and 401K Contribution

The traditional 401K and IRA are the oldest plan types.

They’re traditional because they’re the default and behave like what we had described above: you delay paying income tax on the money until withdrawal.

So for both the traditional 401K and IRA, if you put money into a traditional plan for that year then you pay lower income taxes during the same year.

Of course, you have to pay taxes on this money when you withdraw it, but the delayed tax payment will allow you to grow from a larger base.

Roth 401K and Roth IRA Contribution

Roth 401K and IRA are recently recent initiatives by the IRA to further help Americans save on taxes.

IRA introduced Roth in 1998. And 401K started Roth in 2006.

Depending on who you are, a Roth plan might be better or worse for you compared to a traditional plan.

For a Roth IRA or Roth 401K, you have to pay income tax on the money you deposit into your retirement plan right away.

But earnings inside a Roth IRA or 401K are able to grow tax-free as the money is then never taxed when you withdraw it after 59 ½.

When you invite is a Roth plan, not only do you defer capital and dividends taxes, you never have to pay them, ever!

This is why you want to invest your Roth money into fast-growing funds knowing you won’t pay taxes on the growth.

And since you can’t pick both the traditional and Roth plan under 401K and IRA, you have to choose.

Many people choose to pick a Traditional 401K plan and a Roth IRA to make allocate fast-growing assets under the Roth IRA and safer assets under the Traditional 401K.

So if someone asks you whether you ought to invest in a 401K or Roth IRA, what is your answer?

Your answer is YES – you should invest in both.

Roth 401K vs 401K Contribution

Many employers do not offer Roth 401Ks, forcing their employees to only choose the traditional 401K plan.

If you don’t see your employer offering a Roth 401K, ask your company whether you would consider offering a Roth option.

However, if your employer does offer a Roth 401K, then you are in luck.

Unlike the Roth IRA, the Roth 401K does not have an income cap – so you can choose to invest your money into a Roth 401K no matter how much money you make.

If your employer offers both Traditional and Roth 401K, you can contribute money to both the Traditional and the Roth as long as the sum of the two does not exceed the 401K contribution limit.

If you do have money in both the Roth and 401K, you can minimize your future taxes by allocating your assets smartly, putting your high-risk, fast-growing investments in your Roth and the less-risky ones in Traditional.

Roth IRA Limits

The Roth IRA is not available for high-income earners.

To invest in a Roth IRA, your modified adjusted gross income has to be less than $124,000.

Therefore, many high-income earners do not qualify for the Roth IRA and must invest in the Traditional IRA instead.

Backdoor Roth Conversion

If you make too much money to invest in a Roth IRA, you can convert your traditional IRA into a Roth IRA through what’s called a Roth Conversion.

This is essentially a “backdoor” method that rich people use to legally buy Roth even though they can’t buy it outright.

The steps to execute a backdoor Roth conversion is dead simple, too.

- Transfer money from your bank to Vanguard to buy Traditional IRA

- Immediately after, you initiate a Roth conversion with Vanguard.

Vanguard has an entire page dedicated to Roth conversion.

You might need to first open a Roth IRA account with Vanguard if you haven’t already. But these are all steps Vanguard will alert you to do as you convert.

There is also a Roth conversion strategy for the 401K, called mega-backdoor, but that’s limited and too complicated to cover during this guide.

401K Contribution Plans for All

401K is by far the most popular retirement plan in America with more than $3 trillion dollars under the 401K defined contribution plan.

However, there are other plans that you can buy for employment, and you might run into them if you work for a government, a nonprofit, a small business, or for yourself.

403(b) and 457 Plans for Nonprofits and Government Employees

The 403(b) and 457 Plans are unique 401K plans for nonprofits (called 403(b) plans) and government workers (called 457 plans)

The 403(b) and 457 plans are also tax-deferred retirement investments and they operate similarly to 401K and IRAs.

With a 403(b) plan, nonprofit employees can invest retirement funds the same way others would invest in your 401K.

And with a 457 plan, government workers, including teachers in public schools, can create custodial accounts that are invested in annuities or mutual funds the same way others do with a 401K.

SIMPLE IRAs and 401K Contribution for Small Business

The SIMPLE type is an IRA plan for very small businesses to easily facilitate retirement savings.

The SIMPLE IRA is like a 401K specifically created for businesses typically would avoid the 401K because it is too complicated to handle.

Compared to a 401K, a SIMPLE IRA’s setup fees are lower and there is only a single form to file with the IRS.

Many small businesses create SIMPLE IRAs for their employees instead of 401Ks.

SEP IRAs and Solo 401K Contribution for the Self-Employed

SEP (Simplified Employee Pension) IRAs and Solo-401Ks are available to self-employed workers and small businesses where typically the owner is the sole employee.

Money invested into a SEP IRA or Solo 401K are tax-deferred and the money is taxed upon withdrawal.

There are no significant fees required to set up for only the owner herself.

If you are a business owner, a SEP IRA or Solo 401K is a great way to contribute to your own retirement.

Pension vs 401K Contribution

You might also work for a company that has a pension. If that’s the case, then you’d contribute money to that pension instead of a 401K plan and when you retire, your pension will provide you income.

Pension is the most popular retirement plan in the United States before the 1980s. But since then, most companies have killed their pensions and instead opted to offer employees 401K plans.

Some large hospital systems, teacher’s unions, and transportation and labor unions still offer pensions to their employees.

The idea of a pension and a 401K is the same.

Except with a 401K, you have to be very motivated yourself to max out your 401K contributions when there is nobody like pension monitoring and forcing you to make good financial decisions.

If you ever ask yourself the question, “should I max out my 401K?” Just know that the answer is always yes.

Should I Max Out My 401K Limit?

People are not taking enough advantage of the greatest opportunities to save money and grow your wealth faster: 401K and IRAs.

While there are 401K contribution caps, most people are not close to maxing them out.

Have you considered how to drastically reduce your lifestyle, boost your savings and income?

Saving is the only way to having a comfortable retirement. There is no shortcut.

Will you max out your 401K contribution this year? Comment below!

What’s Next?

Looking for index funds to invest your money? Read Best Vanguard Funds for Every Stage of Your Life.

Everyone I know is worried about the recession coming. Are you? Read this guide to learn the Psychological Hacks to Win During a Recession

Learn the fundamentals of building a pro wealth mindset that makes money: Want to Make Money? Build a Pro Wealth Mindset First