Today, I’m going to use data to explain when to buy stocks vs real estate as a way to build wealth.

I’ll share the most comprehensive data ever on historical returns of stocks vs. real estate.

Lastly, I’ll break down the exact real estate returns in the past 10 years. I’ll also share the returns from the hottest housing markets, including the Bay Area, to show you why the S&P 500 stocks still beat them all.

This is part 1 of the FatFire House series. Read part 2 here.

Many bloggers write about buying real estate to get rich. These bloggers share their personal experiences and they come from a good place.

But their stories might be biased.

To see if real estate investment is right for you, let’s look at two factors:

- The Opportunity Cost: what else can you invest your money, and whether the alternative is better.

- The Total Costs of Owning a Home: what will eat into your returns, including one-time costs, annual costs, to ongoing monthly costs.

Let’s talk about each factor in detail, starting with the opportunity cost of investing in real estate vs stocks.

Stocks vs Real Estate Historical Returns

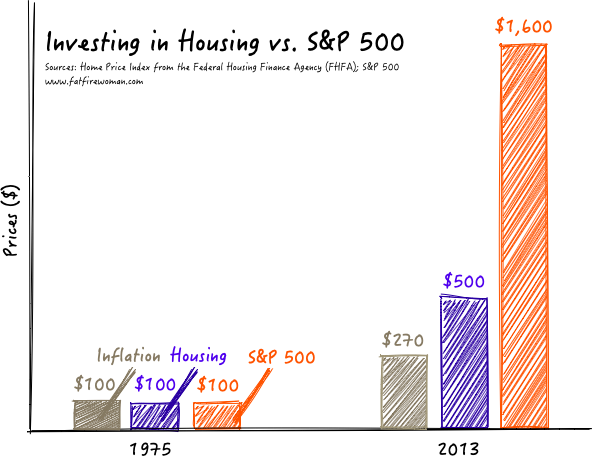

Imagine it is the year 1975 and you have $100.

You can put that money into a house or into the S&P 500 stocks and take it out 38 years later in 2013.

Where would you put the $100 and what would the $100 become in 2013?

The real estate vs stock market chart below answers this question.

- The $100 invested in a house increases to $500 by 2013.

- The same $100 invested in the S&P 500 stocks rises to $1,600.

- Inflation (or cost of living) increased to $270.

Clearly, the S& 500 stocks delivered a much higher return than real estate. In fact, more than 3 times higher over the course of 38 years!

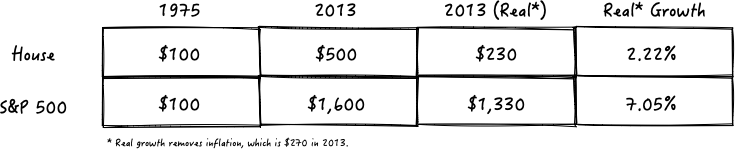

Stocks vs Real Estate: Inflation Adjusted Growth

Since the cost of living (inflation) also increased between 1975 and 2013, let’s subtract inflation to get a sense of “real” returns.

I then tried to annualize the growth rate, subtracting out inflation, to get to a real, annualized growth rate for investing in a House vs. the S&P 500 stocks from 1975 to 2013:

While the house price grew five-fold from $100 to $500, half of that is due to the cost of living increase from $100 to $270.

This leaves the real growth of houses to only $230 ($500-$270) by 2013.

After removing inflation, the real house price rose from $100 to $230, growing on average only 2.2% per year for 38 years.

On the other hand, the S&P 500 stocks index increased from $100 to $1,600 over the same period.

After removing inflation, the value of your S&P 500 stocks grew at 7.05% per year for 38 years to $1,330 in 2013.

By the way, there is nothing special about 1975 or 2013.

Repeating this calculation for any year from the 1940s to the 2020s would’ve given us nearly identical results.

Think about this: stocks deliver more than three times better returns for your money than real estate over nearly 40 years.

This is why real estate is not a good investment compared to stocks, why index funds create millionaires and real estate does not.

The Best Real Estate Markets vs. S&P 500 Stocks

Some of you might argue that the numbers above don’t make sense because the housing price is a national average that includes small towns and depressing cities.

You might argue if we only invested in the hottest real estate markets, such as the Bay Area, at the right time, say the 90s, then for sure, real estate could beat the S&P 500 stocks?

You might be surprised by the answer, so read on.

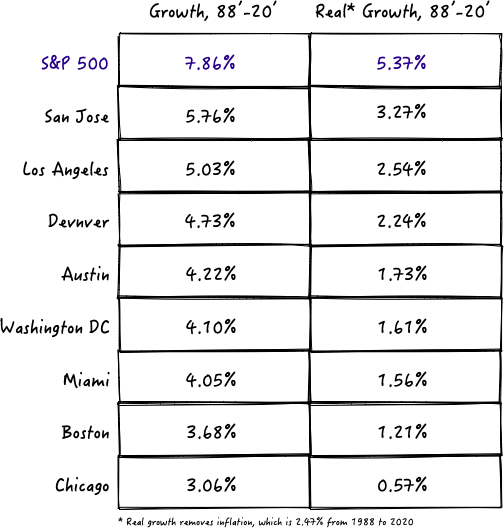

Top 10 Real Estate Markets vs. Stocks

The most detailed, city-by-city real estate data comes from a professor at Yale University called Robert Shiller.

In particular, he developed a Case-Shiller Real Estate Index that is well-known as the most comprehensive real estate data out there.

I’ve analyzed Shiller’s data below to see if the hottest real estate markets during the hottest housing decade could beat the stock market.

The stocks vs real estate graph below show the hypothetical growth of $1 from January 1988 until July 2020 for the S&P 500 stocks vs the hottest real estate markets in the U.S.

Scroll to the right below ← to see the entire stocks vs real estate graph.

Bay Area Real Estate vs Stocks

The stocks vs. real estate graph above showed the S&P 500 stocks blue line grew at a much faster pace than all the lines below, each representing a hot real estate market.

In fact, the S&P 500 stocks outpaced Bay Area prices, represented by the San Jose pink line, the heart of Silicon Valley where housing prices skyrocketed due to the tech boom.

Of all the periods in U.S. history, housing prices grew the fastest starting from the early 90s until the 2020s today.

And there is no place in the U.S. that experienced a faster housing price boom than the Bay Area around San Jose.

But as you can see, even in this “golden” period of real estate growth and even in the hottest real estate market, S&P 500 stocks still won.

True, there was a period in 2008 when San Jose real estate prices briefly outgrew the S&P 500, but the stocks quickly recovered and have since been widening the gap.

Best of Real Estate vs Stocks

Of course, another recession could still hit us and causing stocks to plummet.

But in the long run, data has consistently shown that stocks beat real estate no matter where you buy and when you buy it.

If you think you have a special talent for finding a hot real estate market that can beat the stock market long term, think again.

Looking at data from not just San Jose but Los Angeles, Boston, Chicago, Miami, DC, Denver, and the red-hot Austin, we see that while we are hearing a lot of boom and growth stories from these cities, their real estate prices do not reflect the hype.

So next time you year someone bragging about buying a house in California or any of the hot markets, just know that they would’ve made more money putting that money into the S&P 500 stocks.

And one more thing: I didn’t have enough data to analyze NYC but I’m confident even Manhattan’s real estate prices did not outpace the Bay Area.

Real Estate vs. S&P 500 Stocks: Real Returns

Some people argue that real estate investment is better if you’re doing it for cash flows. You know, getting rental income every month.

These people argue that yes, you might get a lower return than stocks but it’s a very steady income that doesn’t fluctuate with recessions.

Let’s see if this makes sense.

The table below shows the average returns over the past 30 years for the S&P 500 stocks vs the real estate market.

You see that after removing inflation, most real estate returns became less than than 2%.

Even if you want stability and steady cash flows, a 2% growth rate over 32 years is too low to be worth the stability.

And if these hot markets are growing by less than 2%, what about the rest of America?

And you still have to take into account the total cost of ownership.

My conclusion from the market-by-market analysis is that if you want steady cash flow, the only place worth your investment is the San Jose Bay Area in the past two decades.

In the Bay Area, you get a 3.27% return, which is not bad, in exchange for some nice cash flows every month.

Any other real estate market is just not going to worth it. You might as well dump that money into a dividend-rich stock index.

True Cost of Home Ownership

People think buying a house means you don’t have to throw rent money down the drain.

The opposite is probably true.

Let’s take a look at all the costs that go into owning a home.

Home Repairs and Maintenance

When you own a house, you own all of its problems.

You have to pay every time something breaks, from removing a tree struck down by lightning, mowing the lawn, to fixing the toilet or the roof.

Got an ant problem? Pay the terminator. Hot water no longer working? Fix it or spend thousands of dollars replacing it.

On average, home repairs and maintenance costs 1% of your property value every year.

The cost is definitely not steady from month to month or even year to year. Some months you spend nothing.

But things will break, and at some point, you will need to drop thousands of dollars to replace equipment and foundation structures.

If you have a $250,000 house, expect to pay on average $200 a month on home repairs and maintenance.

Homeowners Insurance

Every homeowner needs to buy insurance. Homeowners insurance protects you from both natural and manmade disasters.

A standard homeowners insurance covers fire, hurricane, and maybe even flood, earthquake, and theft.

The cost varies by location and house. For expensive houses, people tend to buy additional umbrella insurance on top of the standard one.

On average, homeowners insurance costs 0.5% of your property value every year.

This means if you have a house valued at $250,000, you’d be paying more than $100 a month on homeowners insurance alone.

Mortgage Interests

When you buy a $500,000 house and only put 20% down, you are borrowing $400K from the bank to live in the house.

The bank will ask you to pay back the $400K with interest. And because the bank holds all the power, the bank will ask you to pay back the interest much earlier than the principle on the house.

In fact, mortgage interests you pay can be 60% of the monthly payment in the first year.

This is why if you buy your house and sell it only a few years later, you are hardly owning the house and thus losing money.

All that money you paid in the first few years is mostly interests, not actual ownership.

Property Taxes

Every state in the United States requires homeowners to pay property taxes.

Property taxes typically costs 1% of your home value.

If you have a home valued at $250,000, you likely need to pay property taxes between $200 to $400 a month, depending on where you live.

You typically pay property taxes once a year at the end of the year, it’s usally thousands of dolars.

Some cities and towns also require you to pay additional education taxes to support the schools in the neighborhood.

Housing Association Fees

If you live in a condo, a coop, or a special neighborhood, there are additional fees you have to pay every month to the association.

These fees go toward roads, snow removal, hiring a doorman or staff, or other general maintenance of your building and community at large.

Housing association fee costs another 1% of your home value.

According to research by Trulia, the average housing association fee is $330 a month, ranging from $100 on the low end to $700 on the higher end.

Utilities

If you live in an apartment, you typically only have to pay for electricity and internet and have some utilities like water or gas covered by the landlord.

But if you live in a house, you pay for everything, from natural gas, electricity to water, garbage disposal, recycling, and any cable and internet.

Utilities cost around 1% of your home value.

An average U.S. homeowner spends $2,000 a year on utilities, which is over $150 a month.

Realtor Fees

Last but not least, you also pay for realtor fees when you buy or sell a house!

A lot goes into buying a home, from the initial set up, listing, and showing to potential buyers all the way to conducting detailed inspections and closing a contract.

The seller typically pays 6% of the home value to sell a house, and the buyer pays 2% to 5% of the home value in closing costs.

In total, about 10% of the house value is paid to the real estate agents just for selling and buying a home.

Real Estate Tax Deduction Myth

Republicans at one point passed a law called SALT, or state and local tax deduction. This law says your property taxes and interests are tax deductible if you itemized your taxes.

A lot of people cite this law as the reason to buy a house because you save money on taxes!

However, this is no longer a valid claim after the 2018 Trump Tax Reform, which made more people elect the standard deduction over the itemized deduction.

In fact, today, only about 10% of the people will itemize their taxes, and most of these people are very wealthy already.

Most of us almost always choose the standard deduction.

And this means the majority of us will not benefit from real estate tax deductions.

Loss of Mobility (Psychological Costs)

A final downside of owning a house is that you are less mobile.

Back in the day, this was fine because most people worked for one company their entire lives.

But in today’s age, mobility means faster career advancement or flexibility.

What if in three or five years you want to move somewhere to better your career? Or what if you met someone in a different city?

And if it’s better for your child to attend a different school?

What if you need to downsize after getting laid off?

Maybe you want to travel the world with your family for 12 months?

Whose dreams are you fulfilling when you buy a house and what dreams are you giving up?

Is owning a house the true freedom you want?

Average Monthly Cost of a Home

It is expensive to own a home.

All in all, you should expect to pay 2% to 6% of your home value every year toward insurance, repairs, maintenance, taxes, and additional fees on top.

I’ve estimated below what total monthly costs might look like for owning a home of various values.

Some of these costs you pay on a monthly basis whereas others you pay every year or even every decade. So these are just the average.

| $/Month | $250K | $375K | $600K | $850K | $1,250K |

|---|---|---|---|---|---|

| Low | $420 | $630 | $1,000 | $1,420 | $2,080 |

| Median | $830 | $1,250 | $2,000 | $2,830 | $4,170 |

| High | $1,250 | $1,880 | $3,000 | $4,250 | $6,250 |

These costs add up and could be costs that you could also invest in the stock market instead.

Never Buy a House?

Look, I’m not saying never own a home.

And don’t get me wrong.

Real estate is a great way to become rich if you are a professional real estate developer. Real estate developers like Stephen Ross to Zhang Xin became billionaires from building large apartments and iconic buildings.

But even professional real estate developers fail. And most importantly, you are not a professional.

You are simply buying a home to live in. So don’t treat your house as an investment.

Seeing it as an investment will cause you to over-think and over-spend.

Your House is a Big Expense

See your house as an expense, a very big expense that is potentially worth it if you are looking to create a lifetime of memories and a place to call home.

Take a realistic look at what you actually want in life and decide if a house is a necessary ingredient toward your ultimate fulfillment and happiness.

Many smart people fall into the trap of buying real estate in the hope to get rich or gather the envy of friends, families and society.

Don’t fall into that trap.

Buy a house and only buy a house if you genuinely believe it will make you happier for the next ten years.

Price-to-Rent Ratio

If you rent a place and wonder if you should buy instead, find out what is the price-to-rent ratio of houses in our neighborhood.

For example, I live in a pretty expensive city where a 3-bedroom apartment goes for $4,500 a month. The same place will probably cost us $1,250,000 to buy today.

$4,500 a month times 12 equals $54,000 going toward rent every year.

To calculate the price-to-rent ratio, I divide the price to own, in this case, $1.25M by the cost to rent, which is $54K, to get 23 as my price-to-rent ratio.

At this point, our family decides to continue renting because 23 as a price-to-rent ratio means I should wait.

And I’ll explain why below.

Buy vs. Rent Rules

The ultimate guideline on whether to rent or buy says you should only buy if your price-to-rent ratio is below a certain number.

The table below shows the guidance. The general rule is that if the price-to-rent ratio is too high, it means the price of these houses is too high compared to the rent they’d be charging.

| Price to Rent Ratio | Buy or Rent Guidance |

|---|---|

| 1 to 15 | Buy – it’s better to buy than rent |

| 16 to 20 | Maybe – it’s risky to buy |

| 21 or More | Rent – it’s not a good decision to buy |

Stocks vs Real Estate is Rent vs Buy

The question of whether to buy stocks vs real estate is a question of whether you should rent or buy. If you rent, you can put all of your money into the stock market, which we know has faster growth.

But you may not be as happy living in a rentaed apartment vs. a house.

Maybe you want to buy anyways. If you do, make sure you are ready and still set up for FIRE.

Follow these home buying rules if you want to maximize your wealth while also live in a house you own.

Rule #1: Find your life’s ambition first.

Are you sure you will plan on living in the same location for the next five years? What about the next ten years?

While your lifes journey to find your purpose may never end, I think it’s important to acknowledge that you should not buy a hoome before you have somewhat of an idea on what your ambitions are in life.

Maybe your ambition is to be a stay-at-home dad, in which case you need to find a wife who makes moey first.

Maybe you are stuck in a job you hate, in which case find out what you want to do with your career first before buying a house.

If you are lost in life, don’t by a house. It won’t solve your problems.

Rule #2: Pay off your debt first.

Why not pay off your current debt first before taking on more debt?

Many people take on a mortgage loan while still paying off their student loans. You can do that, of course, but that’s not the FatFIRE way.

Take care of your credit card debt first, and if you can, also pay off your student loans before you get close to buying a house.

Rule #3: Have One Full Year’s Expenses Covered

Make sure you have one full year’s expenses covered in cash, including cash necessary to pay for my rent or mortgage.

You want to make sure even if you lose your job for a whole year that you can still afford to continue living in the house.

Rule #4: House No More Than 17% of FIRE Goal

Whatever your FIRE goal is, or your net worth goal at which point you will retire, make sure your house value is less than 17% of that goal.

Why? Because you want most of your money to stay in stocks that will grow.

Remember: your home is an expense, NOT an investment! Even though it is the biggest expense you’ll ever make, you still need to keep it low as a percentage of your overall net worth.

A recent Reddit research revealed that the majority of the financially wealth (aka, FatFIRE) people have their primary residence at well below 10% of their net worth.

Given we are the aspiring fatFIRE community, there is a lot of research suggesting that keeping this number at below 17% of your goal will help keep you stay on course to reach your freedom.

Rule #5: Never Spend More Than 25% of Gross Pay on Housing

My last rule is to never spend more than 25% of your gross pay on housing.

My family spends less than 10% of my household gross pay on rent today, but that is because we are making a lot and living very modestly.

When I was young, I shared a 4 bedroom apartment with 4 roommates and paid $750 a month. I was making $60,000 and could’ve afforded an apartment like the rest of my friends.

It was a shitty apartment, but I was able to pay off my student loans faster.

And of course, always pay the 20% down payment. If you don’t have the down payment, you can’t afford to buy. I am not even going to make this into a rule because this should be a given.

Stocks vs Real Estate: Summary

So we know that stocks on average return us 7% per year, whereas real estate, even in the top markets, returns barely 2%.

And then there is all the headache that goes into fixing, repairing, mtainintg, and taking care of a home and its taxes.

The bottom line is that buying a house should not be viewed as an investment.

It is just a home you want to live in and cherish.

I won’t get into the details of renting a house to make money, but suffice to say that the pandemic has taught us that there is no such a thing as stable rental income.

So if you want to buy a house, go ahead! Make sure you can afford to do so by following the five rules I have outlined above.

And then invest the rest of your money into the U.S. stock market.

What’s Next?

Like what you read? Check out part 2 of the FatFIRE series How Much House Can I Afford for Financial Independence?

How old do you think you really are? Find out using the Biological Age Calculator with Instant Results

Spend your money to maximize your health instead. Check out How to Be Healthy and Live Forever

Worth exploring next

- Income Percentile Calculator — Where do you rank?

- Net Worth by Age — How do you compare?

- Retirement Calculator — What’s your real number?

- Rent vs Buy Calculator — Make the math-backed decision

- Best Vanguard Funds — Our top picks for long-term growth